Kenya is accelerating the modernization of its power infrastructure, aiming for universal electricity access by 2030, adding approximately 5.1 million new connections, bringing the total customer base to 15 million. The electricity meter market will shift from a traditional prepaid model to one deeply integrated with smart metering (AMI) and the smart grid, focusing on loss reduction, renewable energy integration, and digital customer service. Kenya Power and Lighting Corporation (KPLC) strategically prioritizes smart meter coverage for high-energy-consuming users and strengthens distribution transformer metering and the Advanced Distribution Management System (ADMS). Millions of new meters are expected to be installed over the next five years, with local manufacturing capacity continuing to expand (e.g., Chinese companies producing hundreds of thousands of units annually). The market size will benefit from the approximately 8.6% CAGR growth of smart meters in the Middle East and Africa. Key drivers include system loss control (targeting a reduction to 15.5%) and the clean energy transition; challenges lie in financing gaps and network coverage. The overall market exhibits strong growth momentum, providing opportunities for Chinese companies in export, localized production, and cooperation.

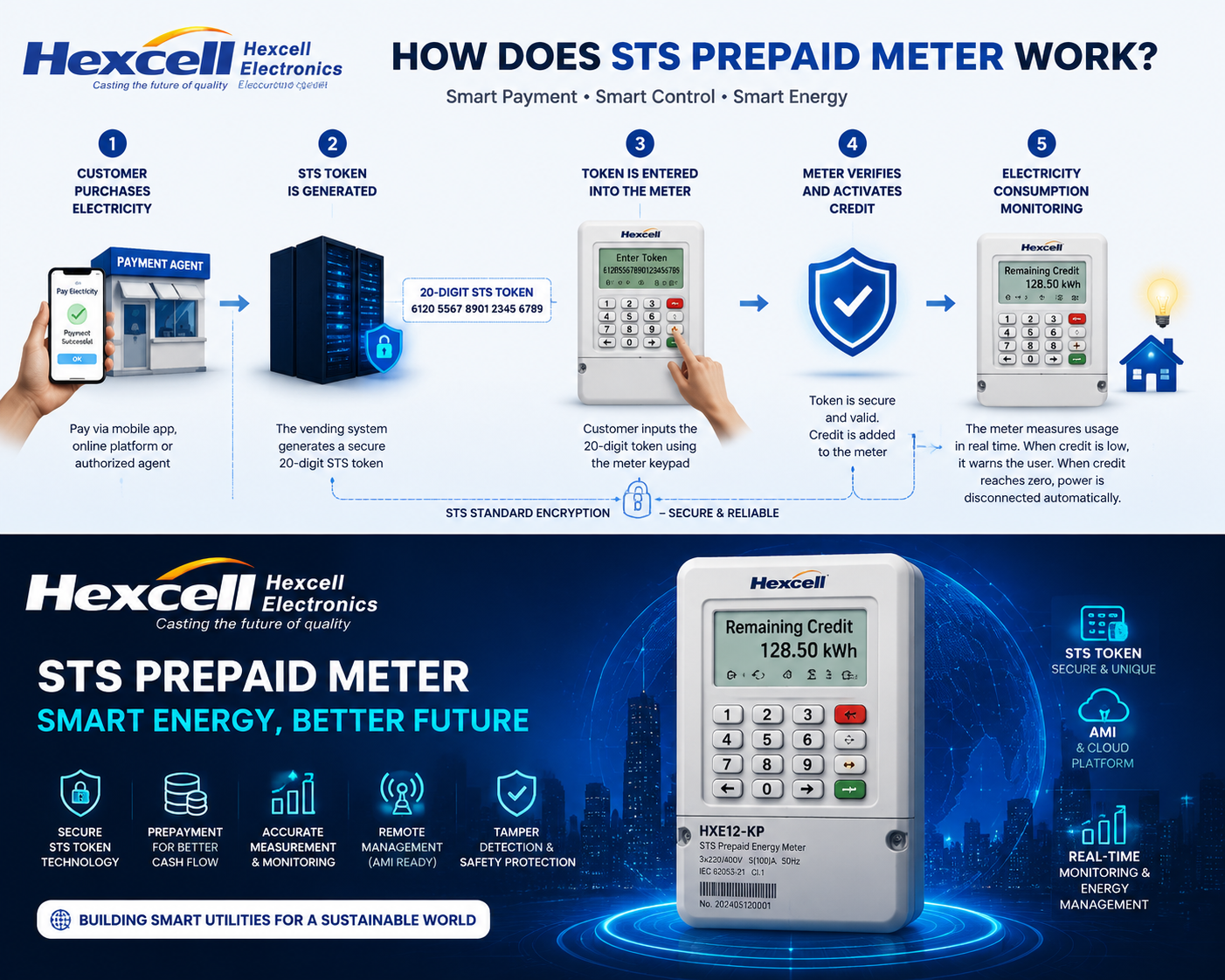

Smart Prepaid Meters in Kenya

Current Status (as of early 2026)

Kenya's electricity access rate has exceeded 76%, and KPLC customers have surpassed 10 million (2025 data). Prepaid meters (token-based) remain the mainstream, covering over 7 million households, primarily serving rural and newly connected areas. Postpaid meters still account for a certain proportion of urban users, but automated meter reading is being implemented in 1.8 million households nationwide using Optical Character Recognition (OCR) technology (full rollout by the end of 2025). Smart meters (AMIs) are mainly deployed in large industrial, SME, and high-energy-consuming residential users (monthly electricity consumption exceeding 200-500 kWh). Although penetration is low, they have proven to reduce electricity theft losses by up to 50%. Distribution transformer and feeder metering are being gradually strengthened to support energy balance analysis. System losses (technical + commercial) remain a major pain point, currently around 18-23%, and smart metering is a key solution.

Kenya Power goes for smart meters to lock out power cartels

Policy and Strategic Framework

Kenya's National Energy Compact Plan (2025-2030) plans to add 5.1 million connections (approximately 4.7 million on-grid) and expand the distribution network by 213,000 kilometers. Key priorities include promoting distribution transformer metering (10,000-30,000 units annually, with a total target of approximately 60,000 units) and deploying smart grid ADMS and relays (500 new units annually). While not mandating smart meters for all customers nationwide, the plan closely links metering modernization with widespread access and reducing losses to 9.3%.

KPLC Strategic Plan (2023/24-2027/28): With operational excellence as its core, the goal is to reduce system losses from 23% to 15.5%. Smart meter penetration for users with >500 kWh will increase from 20% to 100% by 2026/27. Simultaneously, the entire network's ADMS, SCADA, and data analytics systems will be upgraded to support real-time load management.

Other supporting policies: The 2024/25 Net Metering Regulation encourages two-way smart meters (for rooftop solar users); Last Mile Connectivity and the KOSAP project require new connections to be equipped with advanced metering; the e-Cooking National Strategy (KNeCS) will drive demand for electric cooking, benefiting smart prepaid meters.

Key drivers

1, Universal Access and New Connections: 5.1 million new users will directly drive demand for electricity meters, with prepaid models prioritized in rural areas and smart meters prioritized in urban/industrial areas.

2, Loss Reduction and Revenue Protection: Business losses (electricity theft, estimated billing) are a core issue for KPLC. Smart meters and remote power outages can significantly improve cash flow.

3, Renewable energy integration: Geothermal, wind and solar power are expected to account for nearly 100% of electricity by 2030, requiring smart metering to support demand response, peak-valley pricing and net metering.

4, Digital transformation: M-Pesa mobile payment, real-time APP monitoring, and OCR automated meter reading have become standard features, and smart meters will further realize "contactless" services.

5, Local manufacturing and supply chain: Chinese companies are building factories in Kenya (such as producing 400,000 smart meters per year) to reduce costs and support “Made in Africa”.

Development Trends and Forecasts for the Next 5 Years

Installation scale forecast: Combining 5.1 million new connections and upgrades to existing meters, millions of new/replaced meters are expected to be installed between 2026 and 2030. High-energy-consuming users (industrial/SME) will achieve full AMI coverage; new rural households will be dominated by smart prepaid meters. 70-80% of new connections will be equipped with digital metering.

Technological Evolution:

1, AMI smart meters are accelerating their market penetration, supporting 15-minute data interval collection, remote recharge, and dynamic electricity pricing.

2, Full metering of distribution transformers + ADMS builds the foundation of a "smart grid," enabling energy balance and rapid fault location.

3, The growth of bidirectional net metering supports prosumers.

4, Integrate with electric mobility and electric cooking to develop time-of-use electricity pricing and demand-side management applications.

Market structure: Prepaid accounts for 60-70% (mainly low-income groups), while the share of smart AMIs has risen from low to 20-30% (focusing on commercial users). The Middle East and Africa smart meter market is projected to grow from US$25.4 billion in 2025 to US$41.7 billion in 2031, with Kenya, as an East African hub, contributing a significant share.

Localization trend: Chinese companies dominate the supply chain, and the expansion of local assembly will reduce reliance on imports and enhance price competitiveness.

Solar photovoltaic panels in Kenya

Market Opportunities and Challenges

Opportunity:

1, The demand for hundreds of thousands of smart meters annually (new connections + upgrades).

2, PPP financing and green funds support smart grid projects.

3, Emerging data services (energy consumption analysis, carbon credit trading).

4, Chinese companies can participate in the entire value chain, from bidding and factory construction to operation and maintenance.

Challenge:

1, Financing pressures (KPLC debt previously impacted bidding).

2, Network coverage and security (communication in remote areas, data protection compliance).

3, Consumer education and integration with legacy systems (token-to-app transition).

4, Regulatory coordination (ERC and KPLC).

Conclusion

Over the next five years, Kenya's electricity meter market will enter a dual-driven phase of "prepaid adoption + smart upgrades," fully supporting the 2030 goals of universal access and clean energy. KPLC and the national strategy provide a clear roadmap, with loss control and digitalization being the biggest growth engines. Despite financing and infrastructure challenges, the trend is positive. Chinese companies' advantages in technology, manufacturing, and financing make them the preferred partners. It is recommended to continuously monitor KPLC's annual reports and ERC tenders to seize the golden window of opportunity before 2030.